The Spanish PVC Window & Door Market: 2026 Report

This report traces Spain’s PVC window and door market end to end — from raw resin to the finished unit hung in a wall — using customs trade data for the full value chain alongside the domestic industry’s own figures. Trade values are customs values reported in US dollars (the international standard); domestic market figures are in euros. Trade data covers full calendar years 2021–2025; industry figures are the latest available (2023–2024).

1. Foreign trade — the full PVC value chain

The cleanest way to read any window market is through three customs (HS) codes that follow the product down the chain: the raw resin, the extruded profiles, and the finished windows and doors. Here is what each looks like for Spain.

1.1 PVC resin (HS 3904.10) — the raw material

Unlike most countries, Spain is broadly self-sufficient — even a net exporter — in PVC resin, thanks to its domestic petrochemical industry. Resin trade swings with global prices rather than with the window cycle.

| Year | Imports (USD m) | Exports (USD m) | Net imports (USD m) |

|---|---|---|---|

| 2021 | 220.7 | 434.2 | −213.5 |

| 2022 | 254.5 | 373.8 | −119.3 |

| 2023 | 196.2 | 189.7 | +6.5 |

| 2024 | 164.0 | 215.4 | −51.4 |

| 2025 | 191.6 | 222.0 | −30.4 |

Source: UN Comtrade, reporter Spain, HS 390410. Negative net imports = net exporter.

1.2 PVC profiles (HS 3916.20) — the semi-finished frames

Profiles are where Spain depends on imports. Domestic fabricators buy extruded systems — overwhelmingly from German and Belgian makers — then cut, weld and glaze them into windows. Imports run around $80–90 million a year and clearly outweigh exports.

| Year | Imports (USD m) | Exports (USD m) | Net imports (USD m) |

|---|---|---|---|

| 2021 | 76.9 | 42.3 | +34.6 |

| 2022 | 81.0 | 53.1 | +27.9 |

| 2023 | 85.1 | 48.6 | +36.5 |

| 2024 | 80.1 | 47.1 | +33.0 |

| 2025 | 91.9 | 54.9 | +37.0 |

Source: UN Comtrade, reporter Spain, HS 391620.

Where those profiles come from barely changes year to year — and it maps almost perfectly onto the big system brands:

| # | Origin | 2024 (USD m) | Share | 2025 (USD m) | Share |

|---|---|---|---|---|---|

| 1 | Germany | 38.5 | 48.0% | 43.9 | 47.8% |

| 2 | Belgium | 16.3 | 20.4% | 17.0 | 18.5% |

| 3 | Poland | 8.5 | 10.6% | 12.4 | 13.5% |

| 4 | France | 4.3 | 5.4% | 3.6 | 3.9% |

| 5 | Italy | 2.6 | 3.2% | 3.3 | 3.6% |

| — | World | 80.1 | 100% | 91.9 | 100% |

Source: UN Comtrade, reporter Spain, HS 391620 imports by partner.

Where Spain buys its PVC profiles (2025)

Share of profile imports by country of origin

Source: UN Comtrade, reporter Spain, HS 391620 imports by partner, 2025.

| Share of profile imports by country of origin | Value |

|---|---|

| Germany | 48% |

| Belgium | 18% |

| Poland | 14% |

| France | 4% |

| Italy | 4% |

Germany alone supplies nearly half of Spain’s imported profiles; add Belgium and Poland (where several German and Belgian brands run plants) and three countries account for roughly 80%. Poland’s share is the one clearly on the rise — from 10.6% to 13.5% in a single year.

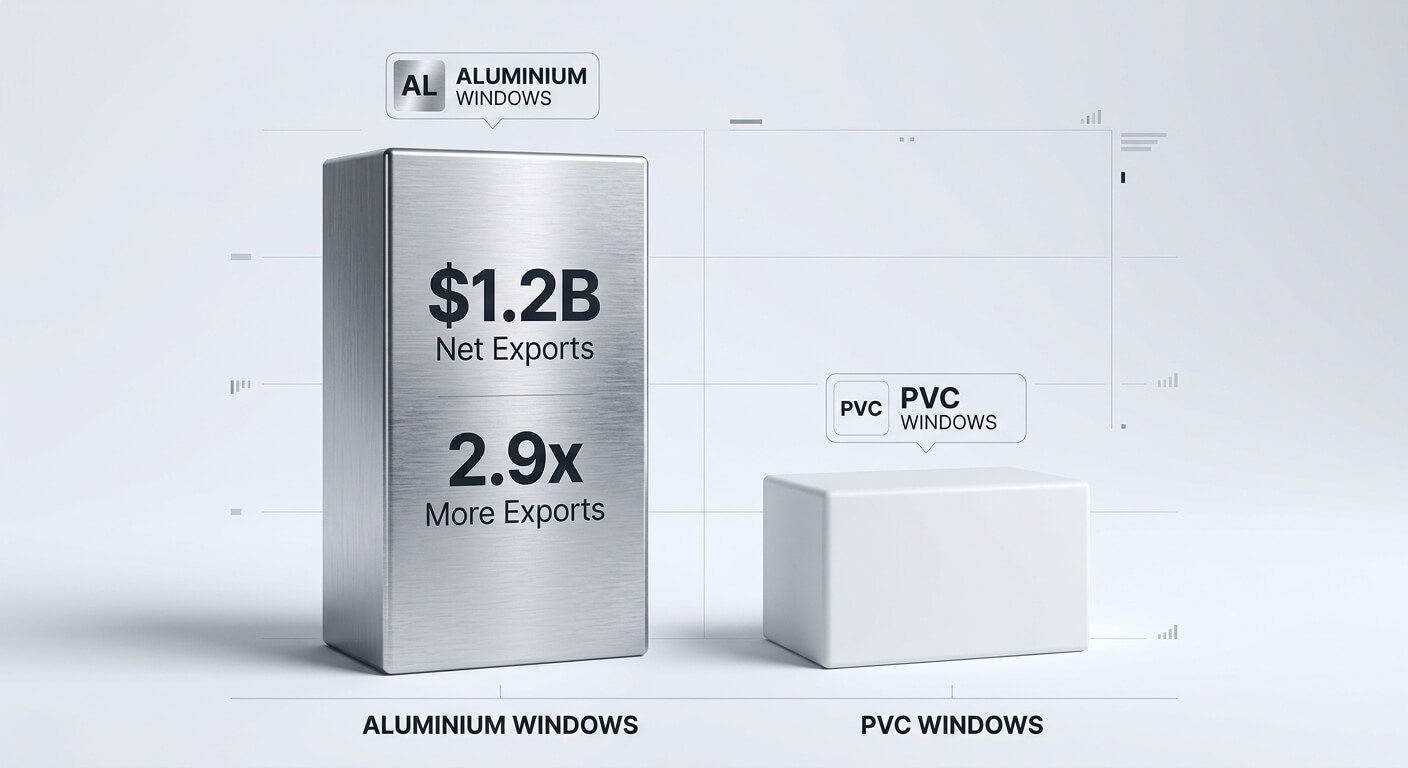

1.3 Finished windows & doors (HS 3925.20)

Spain is a modest net exporter of finished plastic windows and doors — but the headline of 2025 is the import surge: inbound shipments jumped about 38% to roughly $60 million as cheaper finished units, mainly from Turkey and Italy, pushed in hard.

| Year | Imports (USD m) | Exports (USD m) | Net imports (USD m) |

|---|---|---|---|

| 2021 | 33.6 | 46.1 | −12.5 |

| 2022 | 35.7 | 53.4 | −17.7 |

| 2023 | 43.5 | 54.3 | −10.8 |

| 2024 | 43.4 | 57.8 | −14.4 |

| 2025 | 59.9 | 64.2 | −4.3 |

Source: UN Comtrade, reporter Spain, HS 392520. Negative net imports = net exporter.

Finished plastic windows & doors imported into Spain

Customs value of imports, by year (USD million)

Source: UN Comtrade, reporter Spain, HS 392520 imports.

| Customs value of imports, by year (USD million) | Value |

|---|---|

| 2021 | $33.6m |

| 2022 | $35.7m |

| 2023 | $43.5m |

| 2024 | $43.4m |

| 2025 | $59.9m |

Two countries dominate the import side, and a familiar neighbour is climbing fast — Ukraine’s shipments to Spain more than doubled into 2025:

| # | Origin | 2024 share | 2025 share |

|---|---|---|---|

| 1 | Turkey | 37.3% | 37.1% |

| 2 | Italy | 28.1% | 26.7% |

| 3 | Poland | 9.1% | 10.0% |

| 4 | Portugal | 8.3% | 9.1% |

| 5 | Ukraine | 3.7% | 5.7% |

| 6 | Germany | 6.5% | 4.9% |

Source: UN Comtrade, reporter Spain, HS 392520 imports by partner.

Exports, by contrast, are a story of proximity. Almost two-thirds of Spain’s finished plastic windows go next door to Portugal, with France a distant second:

Where Spain ships its finished plastic windows (2025)

Share of finished window/door exports by destination

Source: UN Comtrade, reporter Spain, HS 392520 exports by partner, 2025.

| Share of finished window/door exports by destination | Value |

|---|---|

| Portugal | 62% |

| France | 15% |

| Morocco | 7% |

| Andorra | 4% |

| Neth. | 3% |

1.4 The sector’s trade balance

Put the three codes together and Spain’s PVC value chain is close to balanced — a structural net exporter of resin, a net importer of profiles, and a slim net exporter of finished units. In 2025 the whole chain landed within a few million dollars of zero.

| Indicator (USD m) | 2024 | 2025 |

|---|---|---|

| Imports — resin (390410) | 164.0 | 191.6 |

| Imports — profiles (391620) | 80.1 | 91.9 |

| Imports — windows/doors (392520) | 43.4 | 59.9 |

| Total imports | 287.5 | 343.4 |

| Exports — resin (390410) | 215.4 | 222.0 |

| Exports — profiles (391620) | 47.1 | 54.9 |

| Exports — windows/doors (392520) | 57.8 | 64.2 |

| Total exports | 320.3 | 341.1 |

| Net imports (sector) | −32.8 | +2.3 |

Source: UN Comtrade, reporter Spain, HS 390410 + 391620 + 392520.

2. The domestic market

Trade is only the visible edge; most windows fitted in Spain are made in Spain. The domestic window and light-façade sector turned over an estimated €4.16 billion in 2024, up from about €4 billion a year earlier — a 3–4% gain, per the trade body ASEFAVE.

Spanish window-sector turnover

Estimated annual revenue of window & light-façade manufacturers

Source: ASEFAVE (Spanish Association of Light Façade and Window Manufacturers).

| Estimated annual revenue of window & light-façade manufacturers | Value |

|---|---|

| 2023 | €4.0 bn |

| 2024 | €4.16 bn |

The structure is unusual: more than 10,000 companies, the overwhelming majority micro-businesses of one to ten people. There is no dominant national window manufacturer — the market is a long tail of local fabricators and installers buying profiles and glass from the large system suppliers above.

3. The slow swing from aluminium to PVC

Spain was, for decades, an aluminium country — warm climate, a strong domestic extrusion industry, and habit kept aluminium frames dominant long after PVC took over further north. That is changing. PVC window output reached 1.6 million units in 2024, up 1.5% (ASOVEN), and a 2023 consumer survey found roughly 75% of buyers now lean towards PVC when replacing windows. For context, PVC’s share of the wider European window market hit 36% in 2023 (up from 22% in 2016); Spain still sits below that line — which is exactly why it has the most room left to grow.

4. Who makes the windows

The customs data in section 1.2 isn’t abstract — it is the brand landscape. Nearly half of imported profiles come from Germany and a fifth from Belgium, which maps directly onto the system suppliers Spanish fabricators rely on:

- Kömmerling — German (Profine group); one of the most established PVC brands in Spain.

- Veka — German; its Softline systems are a value-for-money staple.

- Rehau — German; the fibreglass-reinforced GENEO system targets the high-insulation end.

- Deceuninck — Belgian, behind much of that 18% Belgian share, pushing slim aluminium-like aesthetics (iCOR).

- Salamander — long-standing mid-market German system.

In aluminium, the standout is the Spanish heavyweight Cortizo. The competitive story of the decade is these PVC systems converting aluminium’s installed base, one renovation at a time.

5. What’s driving demand

Two engines move this market — new construction and renovation — and both grew in 2024.

What powered window demand in 2024

Year-on-year growth in the two demand engines

Source: Spanish Ministry of Transport (MITMA) construction data, cited by ASOVEN; 2024 vs 2023.

| Year-on-year growth in the two demand engines | Value |

|---|---|

| New-build housing | +16.7% |

| Renovation permits | +7.3% |

Renovation is where the volume already sits. Between 350,000 and 400,000 Spanish homes had their windows replaced in 2023, and crucially one in three did it with a public grant — proof of how decisive subsidies have become in converting intent into a signed contract.

Homes that replaced their windows in 2023

By how the work was funded (≈400,000 homes total)

Source: ASEFAVE. Grant-funded share derived from the reported 'one in three' ratio.

| By how the work was funded (≈400,000 homes total) | Value |

|---|---|

| Self-funded | ~267,000 |

| Grant-funded | ~133,000 |

ASEFAVE puts the typical cost of re-windowing a roughly 100 m² flat at around €10,000 — which is precisely why grants and tax relief swing the decision for so many owners.

6. A renovation backlog measured in decades

The runway is the age of the housing stock. Of Spain’s 25 million dwellings, about 20 million still need their windows replaced — most predate any meaningful thermal-insulation standard. At the current pace of ~400,000 homes a year, ASEFAVE notes it would take around 50 years to clear the backlog. Tightening EU energy rules and Spain’s building code keep raising the minimum a window must hit, steadily pushing owners toward replacement.

7. The bottleneck: subsidies in crisis

Here is what the glossy forecasts leave out. The grant programmes doing so much of the heavy lifting are, by the sector’s own account, jammed. ASEFAVE has publicly denounced a “collapse” in several regions: applications have outstripped the available Next Generation EU funds, payments run 14–15 months late, and there is little transparency about how fast each autonomous community is executing its allocation.

The trade’s demands are blunt: cut the 21% VAT on this work (France applies just 5.5% to energy renovations) and lock in stable income-tax (IRPF) deductions instead of stop-start grant rounds. Layered on top is a labour squeeze — Spain’s broader construction-and-installation workforce is short by hundreds of thousands of workers heading into 2026, and the window trade feels it acutely.

8. Outlook

The fundamentals point up: a 20-million-home backlog, rising energy standards, and a consumer base now defaulting to PVC. The global PVC-window market is forecast to grow ~2.3% a year through 2033 (Ceresana), and Spain — low base, huge renovation pool — should beat that. The brake is administrative, not structural: if the subsidy backlog clears and the IRPF deduction (set to expire end-2026) is extended or made durable, the swing from aluminium to PVC accelerates. Meanwhile, the 2025 import surge is a warning shot — Turkish and Italian finished units, and increasingly Ukrainian ones, are competing on price inside Spain’s own market.

If you’re weighing a replacement, our PVC vs aluminium guide breaks down which actually fits your home and climate.

Sources: UN Comtrade (trade flows, HS 390410/391620/392520, reporter Spain, accessed June 2026); ASEFAVE (sector turnover, company count, renovation volumes, backlog, subsidy programme); ASOVEN PVC (PVC production, consumer preference); MITMA (construction data); FVV (European market share); Ceresana (global forecast).